On 5th July Greeks overwhelmingly voted “NO”; not to Euro, but to crippling Austerity without end in site. It was like a

firm refusal to follow what had not worked by a patient, who had been swallowing medicines administered by the doctor present in the hope of getting better; but was instead getting worse by the day. In fact, in Greek’s case, the patient -that is Greek citizens- did not make a choice to take prescribed medicine, but it was made on her behalf by the “Caregiver” -that is the Greek government. What had the

Troika [IMF/ECB/EC] promised Greece in 2010 when latter was made to swallow the bitter medicine of Austerity? And what condition did Greece find itself in?

Greek’s troubles started at the same time the sub-prime housing mortgage market started imploding in the USA in 2008.

The parallels between the “National” Greece and “Personal” US-Homeowners narratives are uncannily the same. Easy and Cheap Money created through near zero interest rates policy [ZIRP] pursued by the FederalReserve Tzar, Alan Greenspan, for 19 years through 4 successive US presidents, and who oversaw the blowing and busting of the 2000 “.Com” bubble and the blowing of “housing bubble” in the following successive years only to be replaced [just in time to avoid presiding over busting of housing bubble] by Ben Bernanke Ben in 2006.

Greenspan testifying in June 2005, in hindsight infamously, had said:

Although a “bubble” in home prices for the nation as a whole does not appear likely, there do appear to be, at a minimum, signs of froth in some local markets where home prices seem to have risen to unsustainable levels.

What followed instead was sucking out completely of any liquidity from the markets minute the dominoes started falling leading to financial gridlock and finally to endemic recession that won’t be wished away even after seven years of successive quantitative easing [QE] by Fed followed by other central banks like BOJ, then ECB and now PBOC, and by competitive driving down of interest rates into even negative territories by some like ECB, SNB, and DNB.

At the height of the housing bubble less eligible or even ineligible borrowers were lured into home mortgages, which they could have never paid back, through attractive offers of “Zero Downpayment”, carrot of “Capital Appreciation [rising home prices in defiance of long range trend line], waiving or circumventing of “Due Diligence”, and mirage of some “Freebies”. This created the loan portfolio with no hope of payback unless housing market kept up its “inexorable” upward march, which may happen in surreal world of “financial modelling” but never in real life. Not content with this “unbridled casino greed”, the dubious loan portfolio was disguised as high yield collateralised debt obligations [CDOs] and hawked off to unsuspecting but equally greedy investors. This Casino Game was played with great vigour by all major commercial and investment banks led by of course Goldman Sachs. The tide went out when first Bear Stearns failed followed by Lehmann Brothers in 2008. Fed and US government embarked on a gigantic rescue mission ostensibly to save the economy and its citizens from financial catastrophe, but in reality to save the very culprits -To Big To Fail and To Big To Jail- who had brought it on through their Ponzi schemes. The rookie-homeowners faced foreclosure of their un-payable mortgages and the repossession of their homes by the lenders. At least US sub-prime homeowners made their own misinformed choice however foolish. In case of Greece, its citizens did’t even have the luxury of making their own stupid choices. Greece was ineligible to join or would have had to pay heavy fines to the European Monetary Union [EMU] as per the EU Maastricht deficit rules. Lured by the prospect of easy money through common currency Euro, the Greek plutocrats and politicians hatched a conspiracy in partnership with the greatest con artist of all, Goldman Sachs: “Goldman Sachs helped the Greek government to mask the true extent of its deficit with the help of a derivatives deal that legally circumvented the EU Maastricht deficit rules. At some point the so-called cross currency swaps will mature, and swell the country’s already bloated deficit… But in the Greek case the US bankers devised a special kind of swap with fictional exchange rates. That enabled Greece to receive a far higher sum than the actual euro market value of 10 billion dollars or yen. In that way Goldman Sachs secretly arranged additional credit of up to $1 billion for the Greeks. This credit disguised as a swap didn’t show up in the Greek debt statistics“. When the going was good the peripheral members of the EMU or the weaker economies in the zone like Greece, Italy, Portugal, Spain or Ireland lived life well beyond their means buoyed by the Euro. Stronger economies like Germany saw its exports perform strongly on the back of Euro, which was by design weaker than the Deutsch Mark. All boats, good or bad, were lifted when the tide was in until 2008; but when tide went out bad boats were marooned and good ones started complaining about the profligacy of the formers. The easiest way to get over the insolvency of the debtor is to repossess the assets a debtor holds; such as a home and turn the homeowner homeless. Similarly, Greece’s creditors would have loved to take possession of the Greek nation to square of the debts and in the process turning Greeks Greeceless. This may be a lucrative and expedient recourse for the creditor, but is not practical because of the intractable problem of getting rid of large population residing in these lands and the less problematic issue of falling foul of international laws or conventions. Therefore, the less attractive but practical recourse of forcing Greece to tighten belt to save and to pay back to the creditors was chosen with the promise of assistance to avoid sovereign payment defaults provided the prescribed bitter pill was swallowed.

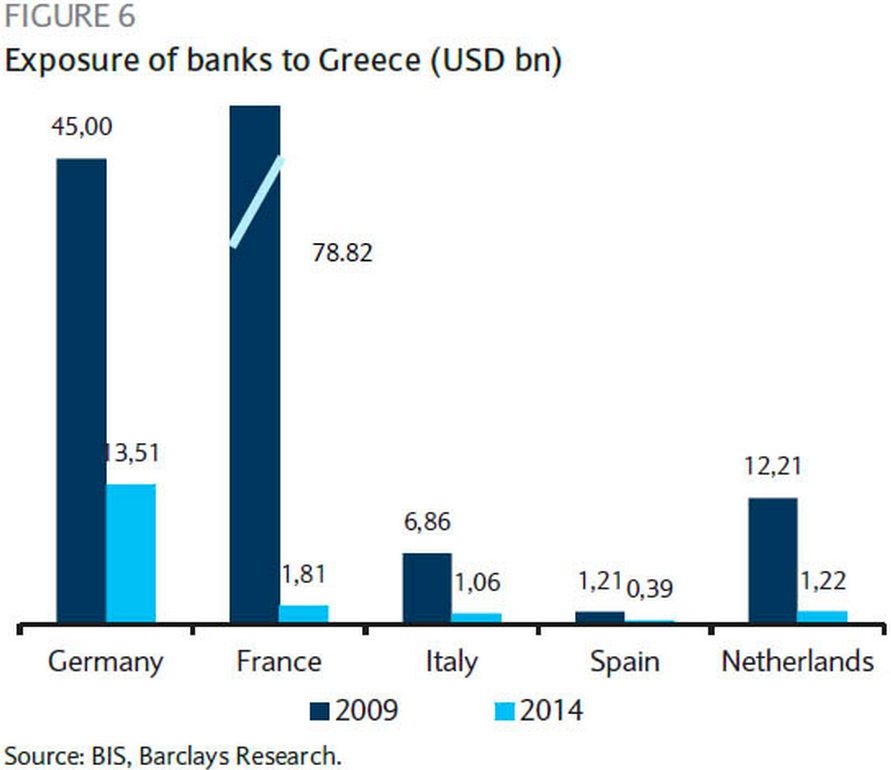

There was one prickly problem too. When the Greek crisis blew up violently in 2008-09, most of the Greek debt was held by private banks; and Financialised, Predatory Capitalism cannot survive unless profits are privatised while the costs are borne by the public. In the disguise of sovereign bailouts [as if they were rescuing the entire Greek population], more than 90% of the money lent to Greece by public institutions like ECB, IMF and EC found its way into the pockets of the private banks. How dramatic was this rescue of private banks would become clear from the following chart that gives exposures of these banks in 2009 and 2014. What a dramatic flow of public/sovereign money, USD 126.11 Billion, into private coffers of private banks just as it happened in USA with Fed’s competitive easing.

So, sovereign bailout was actually in practise private banks’ bailout with public/sovereign money. All the dramatic personae of what economist Steve Keen calls

Eurocrazies [which actually they are not unless seen in ultimate essence] have one thing in common as

Zerohedge.com points out in the following dramatic graphic [see

The Biggest Winner From The Greek Tragedy]. They were/are all connected to Goldman Sachs.

Greece was forced to experiment with Troika’s remedy for 5 long years since its plutocrats and government accepted the “deal”. However, the remedy has not worked as promised and things have got worse and worse rather than the promised initial pain followed by recovery. The fed up Greeks voted the leftist coalition led by Syriza party into power early this year on its promise of ending austerity that was driving down standard of living and driving up unemployment. Syriza wanted a more pragmatic and realistic approach to the solution. If austerity drives down growth and GDP, then paying off debt was going to be difficult, not easier -if one earns less, saves less, then one can only payout less. But, this simple common sense stubbornly escaped the Troika during last 5 months of gut wrenching negotiations; and drove prime minister Alexis Tsipras to seek Greek-referendum; which returned a resounding OXI.

What is the road ahead? Surprisingly,

the lynchpin of the Troika -IMF, which was brought in by EC in 2010, broke ranks just 3 days before the referendum to suggest the “unthinkable”: “

Without a major effort to write off €330bn in loans, the battered economy will remain a financial black-hole for its creditors, locked out of financial markets and ever-reliant on its paymasters to stop it from going bust“. In short, Greek was insolvent unless part of the debt was written off; of course, the “writing off” was to be done by ECB and EU members, not IMF. Would EC or more importantly Germany and France agree to it? Till now, they have made it into a moral issue of “All Debts must be repaid in full, no matter what”. This is not something new as intermeshing of MORALITY and Repaying DEBTS is leitmotif of all cultures and religions since time immemorial [David Graeber-

Debt: The First 5,000 Years]. Germany’s righteous emphasis on morality or repayment of all debts looks tragically scoff-able in the light of its own past as pointed out by

French economist Thomas Piketty in his

interview to German Zeit: “

The German government was in debt after the war ended in 1945 with more than 200 percent of its gross national product. Ten years later it had little choice but the national debt was less than 20 percent of the national product. France succeeded in that time a similar feat. This tremendously rapid debt reduction but we would never have reached with the budgetary resources that we recommend Greece today. Instead, our two countries turned to the second method, the three mentioned components, including debt restructuring. Think. To the London Debt Conference in 1953, canceled on the 60 percent of Germany’s foreign debt and also the domestic debt of the young Federal Republic were restructured“. However, what was good for the German-goose is not considered good for the Greece-gander. Even if Germany and France were to overcome their “moral dilemma”, there is another practical problem: would it open up the Pandora’s Box? If the sovereign creditors were to accept a haircut to have a workable deal, who is to stop the other members like Portugal, Spain, Italy or Ireland from claiming “pari passu” treatment? After all are not all EU members equal? There in lies the Hobson’s choice.

0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0